So, I “budget” a little differently & by that I mean that I don’t do sinking funds or estimate my bills and do the difference. I’ve never really been a fan & for me, I HAVE to know the exact amount, when I need to pay it, & if it’s taken out of my account. With that being said, I’m not the biggest fan of Autopay. The only things I have on Autopay are expenses that are the same amount every single month & are taken out on the same day every month on the same day every single month. I go in every month to check the amount and my account on everything else to make sure there are no extra charges & to make sure everything is correct. Each month, after I pay all of my bills then the remainder (no matter how much it may be) is for saving, spending, paying extra towards debt, groceries, dining out, etc.

Overview

Everyone saves & spends differently because everyone has different financial goals & priorities. A little overview to help understand my budget:

- Fluctuating income

- Student

- Credit Card Debt

- Building credit

- Aggressive Savings

- Dave Ramsey Baby Steps/Debt Snow Ball

Accounts

To understand how I pay my bills, I need to explain how my accounts are set up.

BANKING

I have 3 Checking Accounts, 2 Savings Account, & 1 Certificate of Deposit (CD):

- Main: This is where my Direct Deposit comes in & EVERYTHING comes out from. I only use 1 Debit Card despite having so many accounts and the debit card is linked to this account.

- Joint: I live with my boyfriend & this is the account that we use to pay OUR bills: Rent, Electric, & Internet. We split everything 50/50 & so this is where I put my half of our bills. We both put at least $800 in our joint account each month, even if we both only need to put less. That way there is enough to cover our bills & we may have extra for any maintenance needed that month (rarely ever happens) or we’ll have extra for the months where electricity is higher due because we live in Texas & need to blast the AC in the summer. So when I’m paying bills, I’ll add up our bills and determine if we need to put more than $800 in the Joint account.

- Bills: This is where ALL of MY individual expenses & bills comes out from: credit card bills, car payment, medical, etc.

- General Savings: This is where I put extra cash if I am saving for something I want like an expensive handbag or shoes, trip, or anything that is going to be more expensive than a daily transaction.

- Emergency Savings: I am working on the Dave Ramsey Steps & this is where my emergency $1,000 is at all times.

- Certificate of Deposit*: I use Certificate’s a little differently as well. I’m a shopaholic & I KNOW I have a problem so I love having Certficate’s where I can save money and not have the option to take it out. My current Certificate is my “main savings” for a House & just to put money to save. I will renew it each time & never withdrawal from it. I actually opened a second certificate last year for 12 months that I was using a my “Birthday Trip Savings.” If I got a bonus, received extra money, or just had extra cash I didn’t spend for the month then I deposited it into that Certificate. After all of my bills were taken out of my Main account then I also deposited any extra cash. For example, if there was 648.90 that was left after everything I needed to pay was taken out then I would deposit (at the least) the $48.90 and just have the $600 for shopping/going out. If there was still money in my Main account that I didn’t need or want for the next month then I would transfer the rest to that Certificate. If I used my debit card & my balance would be $348.96 then I would transfer the 96 cents. IT ALL ADDS UP & the best part is that I couldn’t take the money out until the maturity date. So once the maturity date hit earlier this month I had more than enough to book my flight, hotel, & still have cash to spend on the trip!

* A Certificate of Deposit, or CD, is similar to a savings account except there is a fixed maturity date & specific interest rate. Meaning, this is a savings where the funds aren’t available to withdrawal until the specified date you signed up for & you typically earn a higher interest with a Certificate then you do with a savings. For example, I opened this CD with $500 for 15 months at a 2.230% interest rate & I can add money at all time to save. At the end of 15 months I can either withdrawl, renew, or open a new CD with a better interest rate if one is available. I do these because you can not take the money out & It makes saving SO much easier. One thing to note is that if you’re depositing extra money each month, you need to make sure you’re only depositing what you can afford to live without even with emergencies because you can’t withdrawal the funds if something comes up that month.

Cards

I have 1 Prepaid Card, 2 Visa Cards, & 9 Store Credit Cards.

-

- Prepaid Card*: I treat my prepaid card like cash, so I will transfer my spending money on to my card & use that for dinging out, groceries, online shopping & all of my other spending. That way, just like cash, once it’s gone then it’s gone. I got the Starbucks Prepaid Card because for every $10 you spend you get 1 Star, theres no monthly or annual feels, or reload fees. So I’m also earning rewards while I’m spending the money I was going to spend anyways!

- Visa Card (Main): My main Visa card is through my credit union & it has a high credit limit. I primarily use this card for Autopay’s & emergencies. All of my insurance bills (renter’s, car, & pets) and other bills (streaming, Apple Music) that are the same amount & come out on the same day each month are set up with this credit card to make paying bills easier. When this statement comes in then I just pay it off. This also keeps a running balance on my credit card that helps building credit. All of my other expenses fluctuate each month & I prefer to pay them individually. I’ll also use the card for more expensive occurrences like when I need to pay for textbooks or medical emergencies.

- Visa Card (Secondary): This has a samller limit & I use it for minor emergencies like if I forgot my card and it’s the only one I have, but I mainly use this for gas because I don’t like going inside gas stations.

- Store Credit Cards: I have a lot of store credit cards, but I like to earn the rewards. I know a lot of people think credit cards are “evil” but if you use them wisely then they’re you’re best friend. For the most part, I try to not to spend what I don’t have. For example, if I’m shopping at Target then I will use my credit card at checkout because I get 5% off BUT I will transfer or deposit what I spent into my Bills Checking Account so when my Target bill comes then I just pay it off. During any major sale like the Nordstrom Anniversary Sale then I pretty much max out that card (in all honesty) & work on paying it off monthly. But that’s also normally when I shop the most & that sale in particular happens once a year so I also anticipate paying that off.

* Why Prepaid Card? I used to work at a bank and A LOT of people say that they can’t carry cash or they’ll feel the need to spend it. I’m completely opposite, I will spend everything but cash but it doesn’t help when I want to buy something online. For those who can’t carry cash, pre paid cards are becoming very popular for different reasons. If you feel like using cash and/or your using debit card does not help your financial goals, then you should try using a prepaid card. I haven’t seen one that charges you to use it if you get it through a bank or major company. But make sure you don’t get charged if you go this route.

Bills

JOINT CHECKING ACCOUNT

-

- Rent

- Electric

- Internet

BILLS CHECKING ACCOUNT

- Phone Bill

- Car Payment

- Medical Payment

- Loan

- VISA

- Store Credit Cards

AUTO PAY ON VISA

- Renter’s Insurance

- Streaming

- Apple Music

- Car Insurance

- Pet Insurance (2)

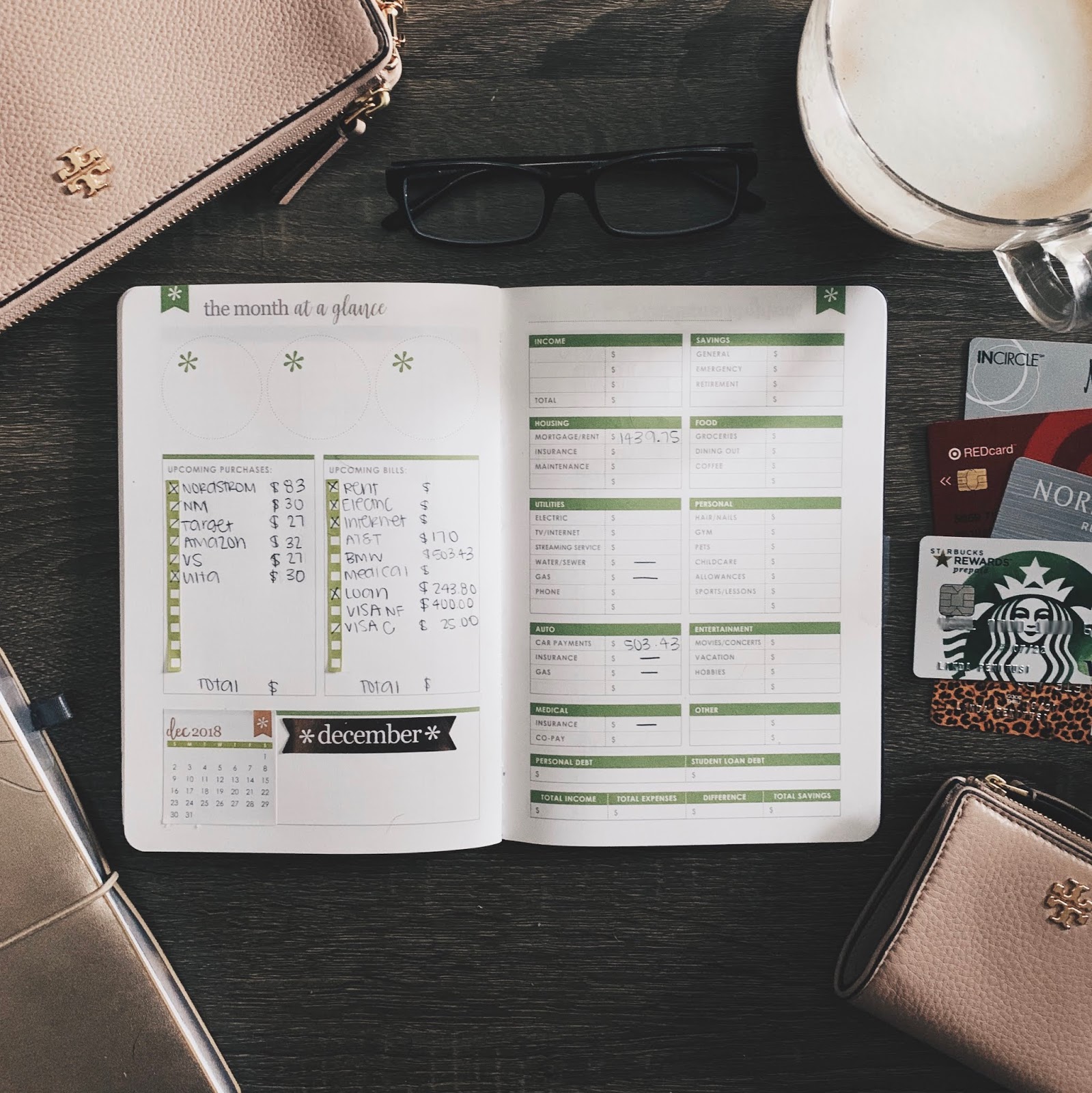

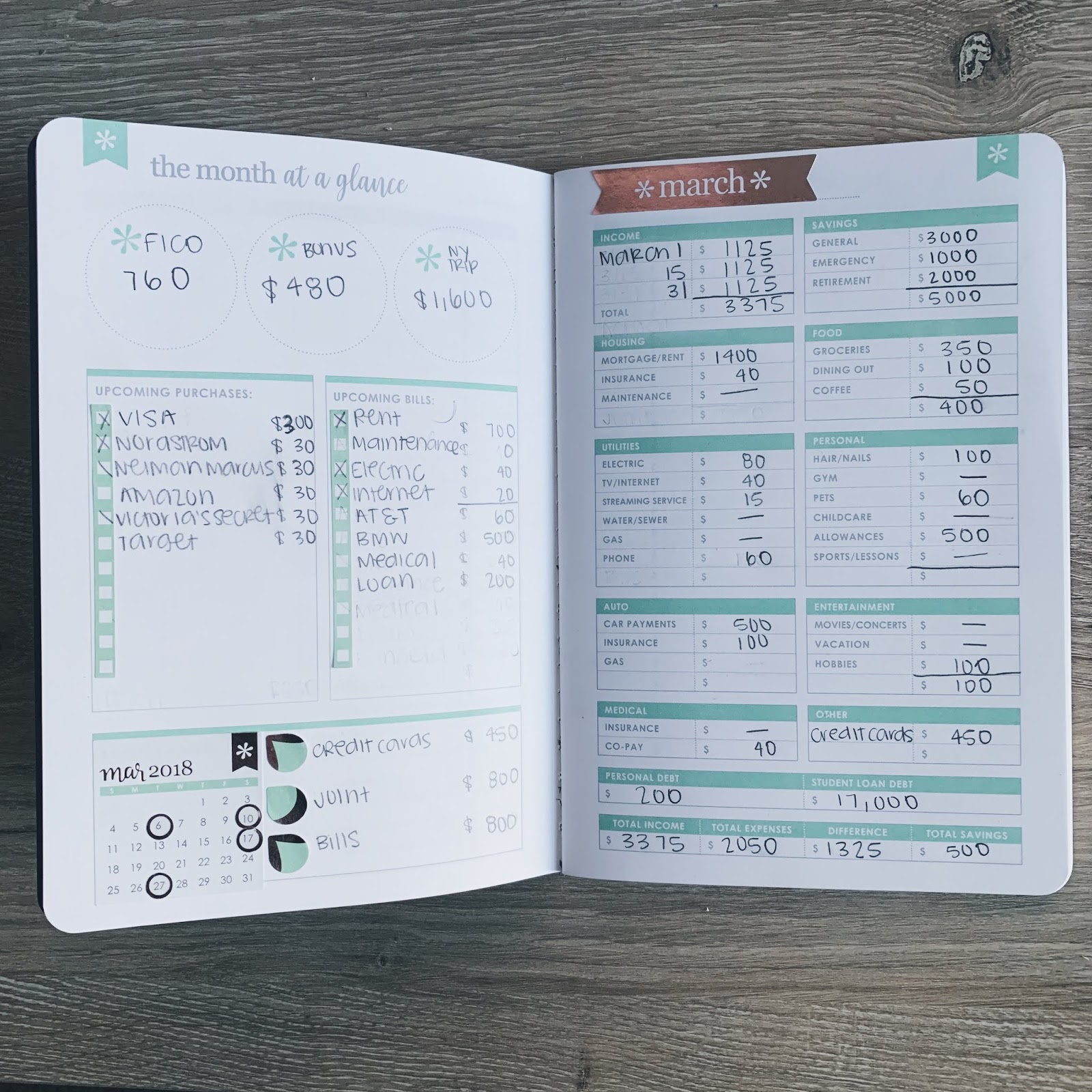

Budget Book

Sample Set UpSET UP:

The Month At A Glance in my Budget Book is where I put EVERYTHING.

PAGE 1:

- 3 Top Boxes: where I track my FICO score or mark expenses that dont occur regularly (like my car insurance occurs every 6 months), tuition, financial aid, etc.

- Upcoming Purchases: This is where I track my store credit cards.

- Upcoming Expenses: This is where I track my utilities & monthly expenses.

- Savings Goals Box: I put a calendar in this box & use this box for a Monthly Summary as opposed to tracking savings.

PAGE 2:

- Income: Total income for each week.

- Savings: Total savings for the beginning of the month.

- Housing, Utilities, Auto, & Medial: I write the full amount due each month, regardless of what I pay.

- Food, Personal, & Entertainment: After I pay all of my bills this where I divide out the amount for each category. Allowances is where I put my cash (since I don’t have kids, it worked out). “Hobbies” is usually my Erin Condren or blogging related expenses.

- Other: I take the total of my credit card payments from Page 1 and write them in here.

- Personal Debt & Student Loan Debt: updated totals monthly.

- Total Income – Total Expenses (Housing, Utilities, Auto, Medical, Credit Cards) = Difference (Food, Personal, Entertainment) & Total Savings

PAYING BILLS:

As different statements come in I put the full amount due on Page 2. Then under The Month at a Glance (first page), I will write the amount that I am paying either the amount due, my half of a bill (rent or bills I split with my boyfriend) or extra towards a credit card. I write what is due on the right to keep accurate records & I want to make sure that the amount needed to be paid is covered. Under Upcoming Purchases & Upcoming Expenses, I have the check mark box stickers that I put a “/” in the box when I transferred the money into the account that I use to pay the bill & then I turn it into a “X” when it is paid.

For example, in the sample pages of my Budget Book, I put that rent was $1,400 under Housing on Page 2. Because my boyfriend & I split rent then I would only pay $700. So on the first page under “Upcoming Bills” I put “Rent $700.” There’s a “X” in the box meaning it’s completely paid. Under “Upcoming Purchases” where I put my store credit card bills, there’s a “/” in the box meaning I put the amount I owe ($30) into my Bills Checking Account where it will come out on the due date since its on Auto Pay. Target & Amazon don’t have anything next to it which means I need to put those amounts due into my Bills Checking Account.

PAYING DEBT:

After all of the bills for the month come in then I add the totals of what I owe. The bottom box under The Month at a Glance page is my visual on the total amount that needs to be in each account ($ for Credit Cards, Joint & Bills). Then I will add all of those together for “Total Expenses” on the bottom box on Page 2. The difference is what I have to spend or save for the month. If I’m trying to save for something big or pay a debt off then this is where the money comes from. I have been putting my spending “cash” and grocery money on my prepaid card & then I will focus on paying bills off or saving with the rest! I am currently using the “Debt Snowball Method” to pay off debt. Means that I am making the minimum payments on everything but I am also paying off debt one balance at a time from the smallest to the largest balance.

FAQ

Q: How do you budget in/pay for more expensive items like designer handbags or trips?

A: I make a “fashion goal” each year to buy something I have always wanted. Last year it was a Tiffany’s Charm Bracelet. This year was a Louis Vuitton Neverfull. Next year was supposed to be Louboutin’s for when I graduate with my MBA, but I actually saved enough to buy them this year so my goal for next year will be another designer item (probably either a Gucci Handbag or Moschino Heels, still undecided). Because I make the goal & I know what I want & I know the price, I will either save up the amount to buy it OR save up at least HALF & put the rest on a credit card and then work on paying off the credit card. I save up at least half because it is usually easier to pay off the remainder. I have a savings account for major purchases for that reason. I know I like to shop and I want to be able to buy things I want so having a separate savings account really helps me.

Q: Why do you have so many store credit cards?

A: I try to get one for everywhere I shop because of the rewards. I save SO much because of the rewards I get with each credit card. The most I have ever paid in interest a YEAR (between ALL of my credit cards) was about $50 and I save about $500 at Target a year alone & I earn at least $300 in Nordstrom Notes a year. If you don’t overspend &/or don’t spend what you don’t have then there is nothing scary about credit cards.

Q: What do you do to build credit?

A: Lenders typically like to see that you’ve used a variety of accounts responsibly, they’re paid on time & that you can keep balances below 30% of your limit (on average). So I try to do just that. I make sure every monthly payment is paid. I don’t spend more than 30% of my limit & if I get anywhere close then I pay that down FIRST. I TRY not to spend more than I can pay off by the time the bill comes, but I know myself & I know that’s not always gong to happen. & when that happens, I make sure that I have enough for the monthly payment (not hard its typically like $30 for most of my cards) & that I work on paying that credit card off.

Q: What do you do to save money?

A: Certificate’s of Deposits have been my favourite way to save money, because you can put money in and not take it out until it matures. & that’s when you can actually see the savings grow.

Q: What Dave Ramsey Baby Step are you on?

Baby Step 2: Pay off all Debt using the Debt Snowball. However, I switched step 2 & 3. As I’ve stated before, I’m on a fluctuating income & I want to make sure that I have money saved to pay my bills. SO, I have 3 months of bills (rent to minimum credit card payments) in my General Savings (Baby Step #3) & $1,000 in Emergency Savings (Baby Step #1).

Q: What’s your advice for saving and budgeting?

A: Know yourself & know your goals. Everyone budgets, spends, & saves differently so use methods that work for YOU. I am a student with no children so I am going to spend and have different financial goals than someone married with children. Also keep that in mind when you’re watching budgeting videos or reading blog posts on savings (& etc). Being honest with yourself about your spending habits is the best way to create a budget that will actually work for you.